Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Lately we have talked about life changes leading to real estate moves. Sometimes moves are brought on by joyful advancements in life and sometimes they are motivated by hardship. Then there are times when your actual house just doesn’t fit your life anymore and it is time for something different. Whatever might be calling someone to make a move, they also have to assess the affordability.

There are three aspects to affordability: price, interest rate, and income. Price and interest rate will determine your monthly payment, and your income will provide the means to maintain and build your investment. One way I have been able to help my clients strategize affordability with higher interest rates are some creative financing options.

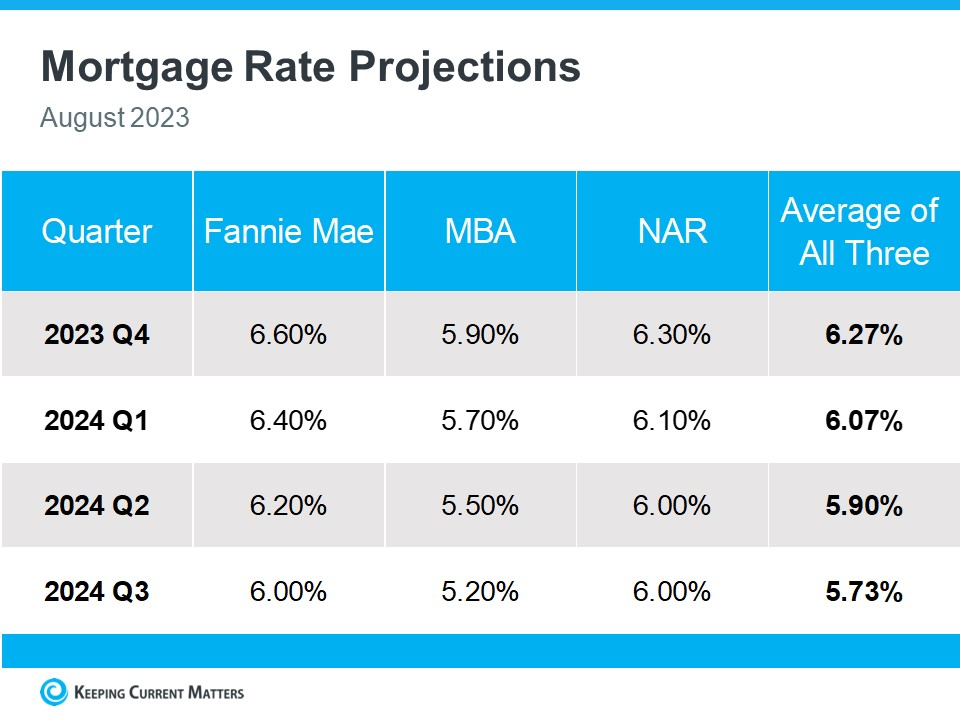

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

Most often a home buyer will procure a home loan with a 30-year term and the current interest rate. In the month of August, the 30-year conventional interest rate averaged 7.25%. While 7.25% is reflective of the average over the last 30 years, it is 2-3% higher than what we have experienced over the last 5 years. According to several experts, rates are predicted to decrease as we finish out 2023 and head into 2024. That also means that it is very likely prices will increase when that happens.

I have helped some of my clients overcome the higher interest rates and secure today’s prices by helping them arrange with their lender an interest rate buy-down. Sometimes we have even been able to get the seller to financially assist in paying for the buy-down. There are two types of buy-downs: a permanent buy-down and a temporary buy-down.

A permanent buy-down requires about 3% of the purchase price to buy the rate down by a point for the 30-year term of the loan. A good rule of thumb to remember is that every 1-point in rate equals 10% in buying power. For example, if the rate is 7% and you are qualified for a home at $800,000, if the rate went down by 1 point to 6% you could now afford $880,000 and have a very similar payment. Another way to look at this is simply the monthly payment itself. An $800,000 purchase with 20% down with a 6% interest rate would save a buyer $420.82 a month vs. the payment at 7%.

A permanent buy-down is a useful tool and so is a temporary buy-down. It is actually one of the most powerful tools in today’s market. It costs far less than a permanent buy-down and with rates predicted to decrease over the next 12-18 months as inflation settles, you could easily find yourself in a position to refinance.

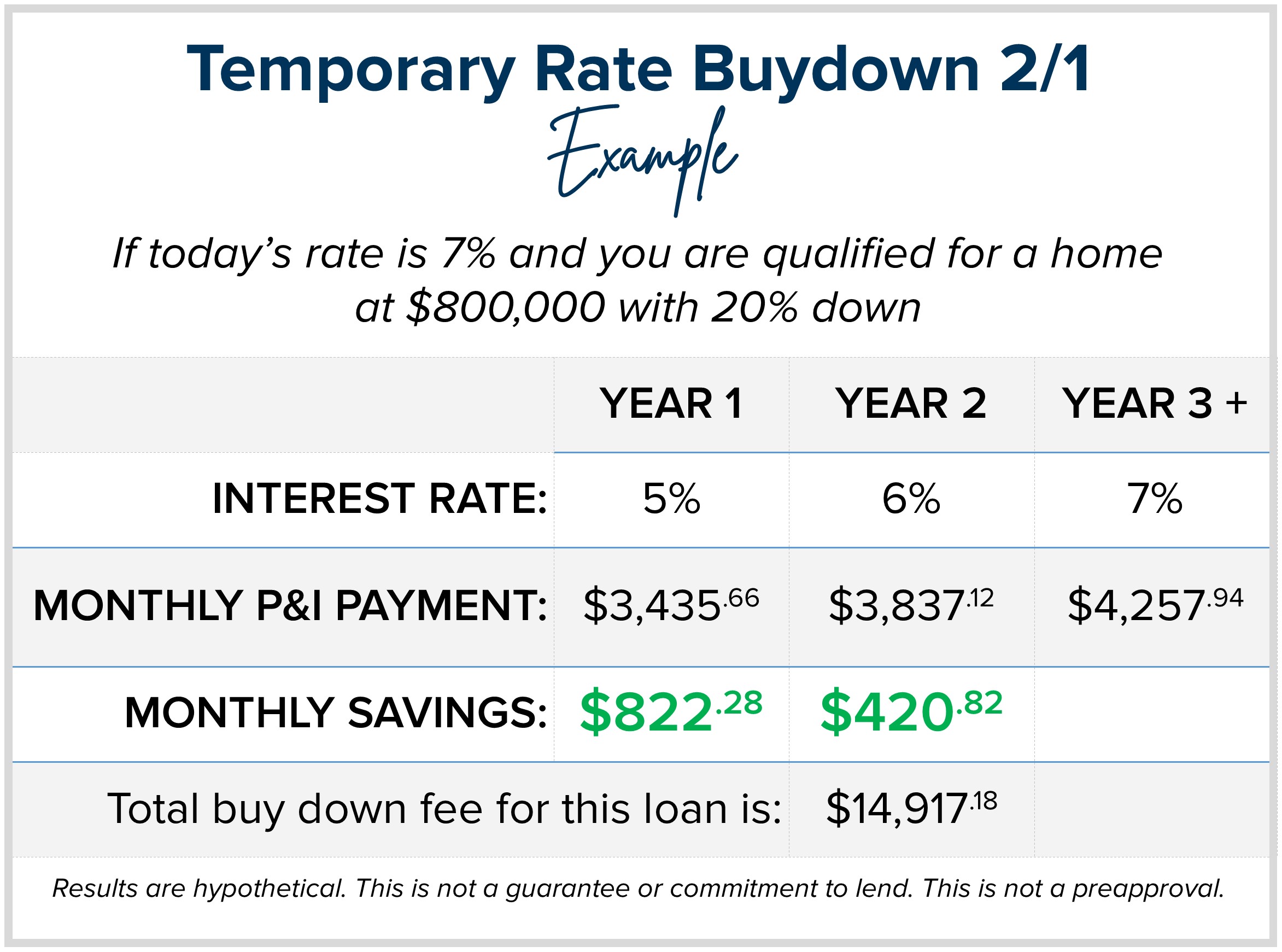

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

Here is an example, let’s say you are shopping for a house and have the same $800,000 budget and a 20% down payment with today’s rate of 7%. The monthly principal and interest payment would be $4,257.94. You could do a 2-1 buydown (2 points lower in year one and 1 point lower in year 2) which would have your payment in year one be based on an interest rate of 5% with a monthly principal and interest payment of $3,435.66 – a savings of $822.28 a month. For year two, the monthly principal and interest would be based on 6%, resulting in a monthly payment of $3,837.12, a $420.82 savings. The total savings in monthly payments with the 2-1 buy-down over the two years would be $14,917.18.

The roughly $15,000 in monthly payment savings is paid upfront at closing and in some cases paid by the seller. The buyer still needs to qualify based on the 7% interest rate as the payments will convert to the payment based on the 7% in year three moving forward. The strategy here is to never have the payment increase to 7% amount because the buyer plans to refinance when rates come down and will permanently fix their rate below 7%. A bonus is that if the entire $15,000 credit has not been used yet, in some cases those funds can be applied towards the refinance.

This strategy has been effective in helping buyers secure a monthly payment that is more affordable so they can make a move now based on life’s needs and wants. It also helps them secure today’s prices. If we find a home that has had a little longer market time, a home seller is likely to assist with the $15,000 credit vs. reducing their price by 3% to accommodate a lower payment for 30 years. The temporary assistance in reducing the payment for 1 to 2 years is a viable tool for both the buyer and seller to create a win-win.

I felt it was important to bring these options to light and to encourage people to not just take today’s market at face value. Creativity, collaboration, and calm have led to some of the most rewarding sales this year for both buyers and sellers. When people logically work together to accomplish moves in an environment that seems difficult, they find success. Ultimately, I am here to help my clients match their real estate to their lives despite where the rates are today.

I love rolling up my sleeves and creating a plan to help my buyers and sellers accomplish their goals. It is my mission to help keep my clients informed and empower strong decisions. If you or someone you know are curious about how today’s market matches your needs, please reach out.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you to everyone who pitched in during the Summer Food Drive! Through your generosity, we collectively donated $3,060 and 1,503 pounds of food to Volunteers of America Western Washington food banks! This is all going directly into our communities to help our neighbors in need.

Thank you!